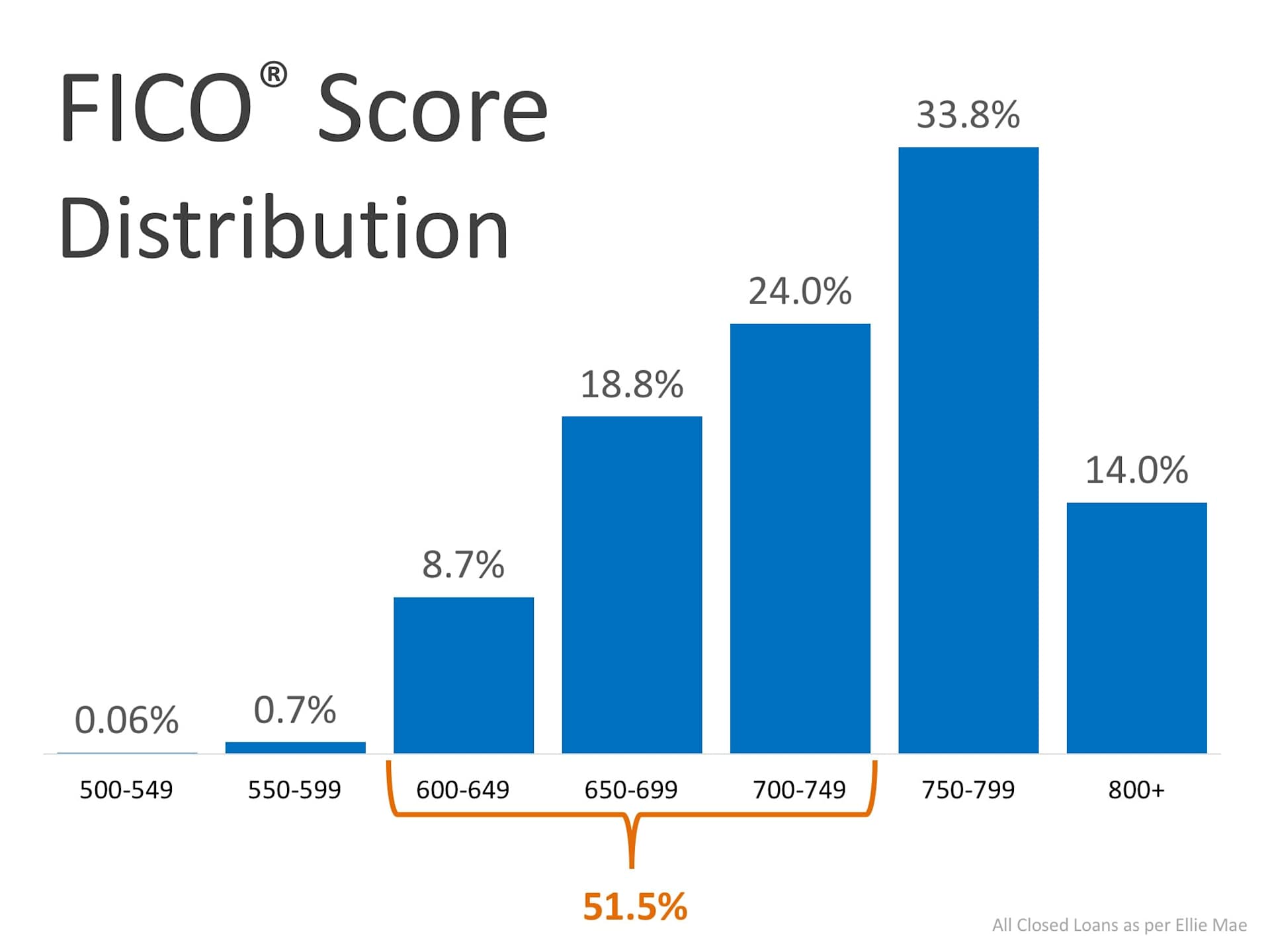

You Do Not Need 20% Down to Buy Your Home Now!

Alexander Trevino June 26, 2018

Alexander Trevino June 26, 2018

Home Staging Secrets That Capture Buyers in Silver Lake’s Competitive Market.

Understanding the Role of Real Estate Agent Representation in Silver Lake’s Competitive Market.

Ask Your Agent to Find Homes with Features You Want.

Insight Into the Silver Lake Home Search.

Transform your Silver Lake home into a restful sanctuary.

A complete guide to transforming your outdoor space into a high-value asset.

A guide for homeowners who want a refined, high-functioning garage.

Your roadmap to showcasing sophistication and securing premium offers.

A guide to finding the kitchen where your creativity can truly shine.

We pride ourselves in providing personalized solutions that bring our clients closer to their dream properties and enhance their long-term wealth. Contact us today to find out how we can be of assistance to you!